The convergence of Product Lifecycle Management (PLM) and Enterprise Resource Planning (ERP) systems is reshaping the landscape of U.S. manufacturing. Driven by rapid advancements in digital technologies, the imperative for integrated supply chains, and the demand for real-time data sharing, the traditional boundaries between PLM and ERP are dissolving. This integration promises significant gains in process efficiency, data governance, and cross-functional collaboration, but also introduces complex challenges related to software interoperability, organizational change management, and workforce readiness. As manufacturers navigate this transformation, those who successfully integrate PLM and ERP systems are poised to achieve a sustainable competitive advantage through enhanced agility, innovation, and operational resilience.

The U.S. manufacturing sector is undergoing a profound digital transformation, with PLM and ERP systems at the core of this evolution. Historically, PLM managed the upstream processes of product design and development, while ERP focused on downstream operational and transactional activities such as procurement, inventory, and finance. However, the rise of automation, artificial intelligence (AI), Internet of Things (IoT), and cloud computing has created a demand for seamless data flow across the entire product lifecycle, from ideation to delivery and service. Enhanced integration is further propelled by the proliferation of smart factory technologies, which rely on real-time exchange between design, planning, and execution systems to identify bottlenecks, adjust schedules, and ensure traceability throughout the production process. Industry leaders are localizing supply chains, leveraging digital twins for simulation, and adopting blockchain for auditability, all of which necessitate a unified architecture capable of synchronizing data across traditionally siloed PLM and ERP domains 1 2.

Manufacturers are also adapting to shifting consumer demand and supply chain volatility by embracing more agile, modular organizational structures powered by integrated digital systems. These transformations not only optimize internal processes but enable diversification of supplier bases, faster responses to disruptions, and better compliance with complex regulations. As digitalization deepens, operational models now require PLM and ERP to orchestrate workflows in tandem, dissolving once-rigid boundaries in favor of a seamless, enterprise-wide “digital thread” that connects concept, engineering, production, and business operations 3 4.

How is the market organized?

The convergence of PLM and ERP systems is evident across various manufacturing segments, including automotive, aerospace, electronics, consumer goods, and industrial equipment. Large enterprises, often with complex global operations and legacy IT infrastructure, are leading the adoption of integrated digital platforms, investing heavily in cloud migration, IoT-based process monitoring, and AI-powered analytics to transform both PLM and ERP into unified, intelligent solutions. For example, in sectors like defense and heavy industry, unified PLM-ERP platforms are now critical for managing compliance, version control, and long production cycles involving multiple international stakeholders 5.

Midsize manufacturers, in contrast, demonstrate higher agility due to flatter management structures and less bureaucratic inertia. Enabled by manageable complexity and moderate investment risk, these companies adopt modular and cloud-based solutions more rapidly, often leapfrogging to the latest integrated platforms without the burden of legacy system upgrades. Regional manufacturing ecosystems, such as those rooted in the Midwest, Southeast, and select “innovation corridors,” are infusing resources into digital infrastructure, workforce cross-training, and ecosystem partnerships to align advanced manufacturing with integrated PLM-ERP capabilities 6 7.

| Segment | Adoption Approach | Key Characteristics | Primary Drivers |

| Large Enterprise | Multi-phase, hybrid-cloud migration | Complex legacy systems, global operations, high compliance and traceability needs | Supplier risk, regulatory pressure, digital twins |

| Midsize Manufacturer | Rapid adoption, SaaS-first | Agile org structure, moderate complexity, quicker pilot-to-production timelines | Process efficiency, flexibility, manageable investment |

| Small Manufacturer | Opportunistic, modular integration | Limited IT resources, focused on cost control, increasing interest in bundled tools | Supplier digital platforms, industry incentives |

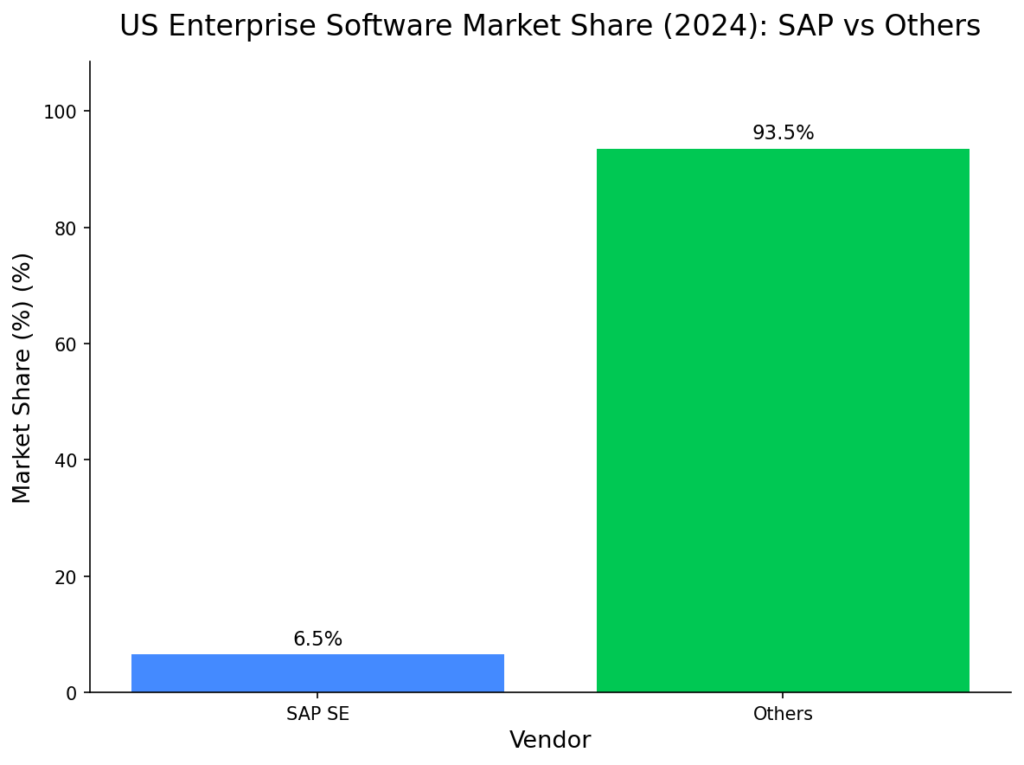

Major enterprise software vendors such as SAP, Oracle, and Microsoft are at the forefront of offering integrated PLM-ERP solutions, often through cloud-based platforms that facilitate real-time data sharing and workflow synchronization 10 11. SAP’s comprehensive suite, Oracle’s industry-centric cloud modules, and Microsoft’s Dynamics 365 ecosystem exemplify modern, scalable architectures with PLM and ERP deeply intertwined. These software leaders continue to broaden their portfolios by merging SCM, CRM, and quality management into unified platforms, further dissolving boundaries and enabling customizable integration for complex manufacturing needs.

Beyond the mega-vendors, a vibrant ecosystem of niche PLM-ERP convergence specialists is emerging, including providers of integration middleware, system orchestration, AI-enabled analytics, and industry-specific solutions. Strategic alliances between consulting firms, system integrators, and software vendors are on the rise to ensure fast, secure, and scalable deployment for companies with unique operational constraints and compliance obligations. For example, Palantir’s partnership with the U.S. Navy demonstrates cross-sector application of data-unifying technology in highly regulated, defense-oriented production settings 5. Additionally, industry-focused vendors like Siemens, Autodesk, PTC, and Dassault Systèmes are deepening ERP integration capabilities within their PLM platforms to compete in this convergent environment 12.

| Vendor | Platform Features | Integration Model | Industry Focus |

| SAP | S/4HANA, SAP PLM | Unified cloud & on-premise | Discrete and process manufacturing |

| Oracle | Cloud ERP, Agile PLM | Pre-integrated SaaS modules | Industrial, aerospace, pharma |

| Microsoft | Dynamics 365, integration APIs | Modular cloud-first | Midsize, multinational, cross-sector |

| Siemens | Teamcenter, MES, Opcenter integration | Deep vertical integration | Automotive, energy, electronics |

Future Forecast

Over the next three to five years, the convergence of PLM and ERP systems is expected to accelerate, driven by continued digital transformation and the proliferation of AI-powered tools. Modular, cloud-deployed platforms will dominate, allowing even resource-constrained manufacturers to participate by investing selectively in the capabilities that drive the most business value 4. Real-time process automation will proliferate across both engineering and operations, as digital threads—extending from concept to end of product life—become standard. Companies will increasingly integrate AI assistants into workflows, supporting design automation, compliance monitoring, supplier collaboration, and real-time corrective action 16 14.

A primary challenge will remain the digital skills gap, as integrating and maintaining these systems will require multidisciplinary teams proficient in automation, analytics, change management, and operational technology. By 2026, industry analysts project that manufacturers who invest strategically in organizational flexibility, continuous workforce training, and comprehensive data governance will emerge as leaders, unlocking both superior financial performance and the ability to respond rapidly to evolving market, regulatory, and supply chain conditions 19 7.

Strategic Insights

The blurring of PLM and ERP boundaries is not merely a technological shift but a strategic imperative for U.S. manufacturers. Integrated systems enable end-to-end visibility, faster time-to-market, and enhanced responsiveness to supply chain disruptions and regulatory changes. Success increasingly depends on not just technology investment, but on transformation in organizational culture, process agility, and the creation of multidisciplinary teams that exploit convergence to break down legacy silos and foster innovation. Midsize manufacturers stand out due to their ability to adapt quickly, supported by manageable complexity and strategic resource allocation, giving them an edge in deploying holistic digital platforms that integrate PLM and ERP functionality 7.

Moreover, firms that embrace rigorous change management, continuous upskilling, and stakeholder engagement are better positioned to sidestep the frequent pitfalls of stalled digital integration. Best-in-class companies act early by establishing governance frameworks, scenario-based planning, and outcome-driven adoption metrics—making digital convergence a catalyst rather than a risk.

Recommendations

Prioritize Integration Strategy: Manufacturers should develop a clear roadmap for PLM-ERP integration, focusing on scalable, cloud-based solutions that support real-time data sharing and collaboration, and leveraging modular approaches to pilot value in high-impact areas before full-scale roll-out 4 15.

Invest in Workforce Development: Upskilling and reskilling programs—not just technical but change-leadership skills—are essential to bridge the digital skills gap and sustain adoption. External partnerships with regional training centers, community colleges, and industry consortia can help scale workforce readiness 19.

Enhance Data Governance: Implement robust frameworks for data quality, security, and compliance. This includes continuous auditability, strict access controls, and readiness for future regulatory requirements. Establishing a “single source of truth” across engineering and business operations is critical to maximizing integration value and risk mitigation 11 14.

Foster Cross-Functional Collaboration: Proactively break down silos via cross-departmental teams, co-located innovation labs, and digital collaboration tools. Iterative process mapping workshops and agile workflows anchored in integrated PLM-ERP platforms foster alignment, resilience, and sustained innovation 9 21 22.

Adopt Change Management Best Practices: Engage stakeholders early and often, transparently communicate integration goals, benefits, and timelines, and continuously measure adoption. Use peer champions and iterative training models to overcome resistance and foster organizational buy-in. Anticipate and plan for the human experience of change, not just the technical rollout 20 23 24.

Appendices

- [1] 2025 US Manufacturing Outlook: Challenges, Trends, & Supply Chain Resiliency —> Google

- [2] Impact of Industry 4.0 on Product Lifecycle Management – Automation Alley —> Google

- [3] ERP PLM Integration: Breaking the Wall for Industry 4.0 – IndustryX.ai —> Google

- [4] Product Lifecycle Management (PLM) in 2025: Trends, integration, and business value —> Google

- [8] PLM Priorities for Large Manufacturers — Analysis of 2024 IDC MarketScape Results —> Google

- [9] 31-33 Manufacturing in the US Industry Report.pdf —> IBIS World

- [10] 51121 Software Publishing in the US Industry Report.pdf —> IBIS World

- [11] 51121C Business Analytics Enterprise Software Publishing in the US Industry Report.pdf —> IBIS World

- [12] Convergence Data Partners with Siemens PLM Software —> Google

- [13] 51121C Business Analytics & Enterprise Software Publishing in the US Industry Report.pdf —> IBIS World

- [14] PLM in 2025: What’s Driving Change in Manufacturing – YouTube —> Google

- [15] ERP Trends 2025: How PLM Software Enhances Business Solutions —> Google

- [16] Future Trends in PLM: What Engineering Leaders Need to Know – SPK and Associates —> Google

- [17] ERP and Product Lifecycle Management (PLM): Integration, Impact, and Benefits Explained —> Google

- [21] PLM and ERP: Why and How to Integrate These Business-Critical Systems – pdsvision —> Google

- [23] How to Do Change Management for PLM Implementation – Best Practices for Success —> Google

- [5] Palantir Wins U.S. Navy Contract For Nuclear Submarine Fleet. Potential Bigger Than Maven?

- [6] 7 Trends Shaping Economic Growth Across the U.S. —> Dow Jones

- [7] Why Midsize Companies Are Best Positioned to Thrive in the Age of AI —> Dow Jones

- [18] CEOs’ Biggest AI Fear Is Surprisingly Old School —> Dow Jones

- [19] The Skilled Worker Shortage May Hit Hard in 2026 —> Dow Jones

- [20] Change Management Is Broken. These 4 Numbers Explain Why —> Dow Jones

- [22] Finding Calm in Chaos: How Leaders Can Thrive Amid Industry Uncertainty —> Dow Jones

- [24] Leaders Must Stop ‘Doing’ AI and Start ‘Using’ It —> Dow Jones